Reverse liquidity tightening

Financial Express, 19th September 2013

Reserve Bank of India took a number of steps to tighten liquidity and raise rates in mid-July. As a consequence of these steps interest rates today are up to 400 basis points higher than they were in the beginning of July. While this rate hike is reminiscent of the rate hike of 200 basis points by Bimal Jalan on January 16, 1998, when he stepped in to defend the rupee in the Asian crisis, such a steep policy rate hike has never been done before. Moreover, it was implemented through non-transparent and quantitative measures that have damaged the operating procedure of monetary policy.

While some other emerging markets (EMs) have also defended their currencies with interest rate hikes, it has not been so brutal. It has also been done primarily by raising policy rates and not by breaking down the operating framework of monetary policy.

In its credit policy announcement RBI must first and foremost reverse these steps and restore the operating procedure of monetary policy. Only then can it discuss the stance of monetary policy. No monetary policy designed to manage expectations can deliver any meaningful objectives if rates are raised so sharply and so suddenly. The tightening was supposed to be temporary and so reversing the measures will not damage RBI's reputation for consistency. The current phase of lower pressure on EM currencies offers a window to correct the policy mistakes made in the last two months.

Mid-summer tightening

On July 15, Reserve Bank put in place measures in response to the pressure on the rupee to depreciate. They included raising the MSF rate by 200 bps to 10.25%, restricting the overall access by way of repos under the liquidity adjusted facility (LAF) to R750 billion and undertaking open market sales of government securities of R25 billion on July 18.

On July 23, RBI modified the liquidity tightening measures by regulating access to LAF by way of repos at each individual bank level and restricting it to 0.5% of the bank's own NDTL. This measure came into effect from July 24, 2013. The cash reserve ratio (CRR), which banks have to maintain on a fortnightly average basis subject to a daily minimum requirement of 70%, was modified to require banks to maintain a daily minimum of 99% of the requirement.

On August 8, the central bank augmented its measures to tighten liquidity by announcing the decision to auction GoI Cash Management Bills for a notified amount of R220 billion once every week.

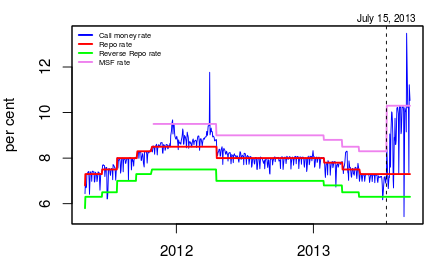

Figure 1: Interest rate defence and breakdown of operating procedure

The announcement of the MSF rate hike sent inter-bank markets into a spin and the weighted average call money rate breached both the upper and lower bounds of the modified operating corridor of monetary policy. This is the first time the RBI has deviated from the ±100 bps fixed width corridor around the repo rate after it announced its new monetary policy in May 2011.

The policy framework

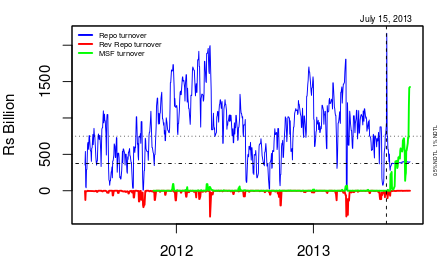

Figure 2: Structural liquidity deficit, rate hike pushes banks from LAF to MSF

RBI announced its current monetary policy framework in May 2011 to move to an explicit operating target, a single policy rate and a formal corridor system with a symmetric 100 bps spread on either side of the policy rate. The single policy rate as per the new operating procedure was the repo rate with the reverse repo being the lower bound of the policy corridor and the marginal standing facility (MSF)/bank rate being the upper bound of the policy corridor, distributed 100 bps below and above the repo rate. The explicit target according to the new operating procedure was the weighted average call money rate which would be targeted to lie within the policy corridor as determined by the prevailing repo rate. The LAF window was recommended to be used up to ±1% net demand and time liabilities (NDTL) of the banking system.The MSF or the penal bank rate was to be used for liquidity operations up to ±2% of NDTL of the banking system.

The LAF has never operated within the set bounds of ±1% NDTL throughout its operational history. Given this operational laxity, banks seldom accessed the penal MSF window. After RBI decided to tightly implement the LAF window operation on July 15 and cut it to ±0.5% on July 23, the entire borrowing from the LAF switched to the MSF given the structural liquidity deficit in the banking system. This correspondingly caused all other money market rates to rise

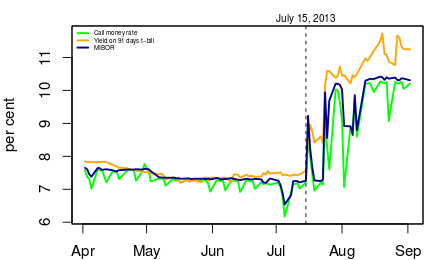

Figure 3: Decoupling of rates, breakdown of transmission

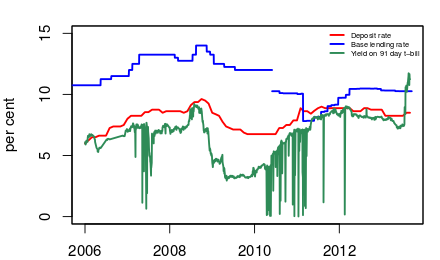

Will lending rates rise?

Figure 4: Lending rates

The secondary market 91-day treasury bill rate captures both the direction of policy rates and liquidity conditions. When compared to the movements of interest rates on bank deposits and lending, it is evident that there is no quick or full transmission of monetary policy. However, as the RBI has noted the behaviour of the banking sector is asymmetrical. When rates ease, banks do not lower rates, but when they rise, they are quick to raise rates. This suggests that if the recent high rates continue, lending rates of banks will rise.

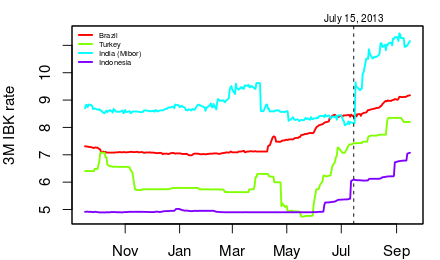

Figure 5: Comparing India to EM peers

When exchange market pressure hit EMs following Bernanke's speech, countries such as Brazil, Turkey and Indonesia also raised interest rates. However, they raised them using policy rates, rather than through quantitative measures that tightened liquidity or by breaking down the operating framework of monetary policy and by much less than India did. India's interest rate defence has been a costly exercise-both, in terms of the up to 400 basis point increase in interest rates that we see today and in terms of the breakdown of the operating procedure of monetary policy that has been implemented by RBI in this effort. RBI must immediately reverse the steps taken and restore the operating framework of monetary policy.

Co-authored by Shekhar Hari Kumar

Back up to Ila Patnaik's media page

Back up to Ila Patnaik's home page